TEL:+86 158 1857 3751

TEL:+86 158 1857 3751

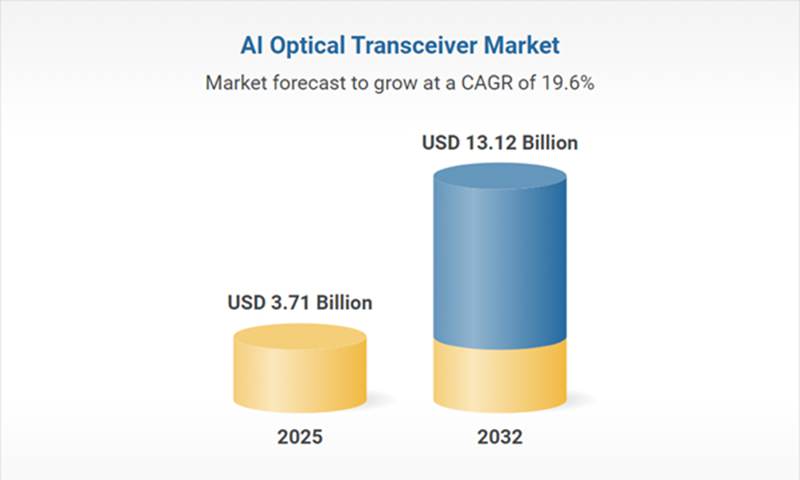

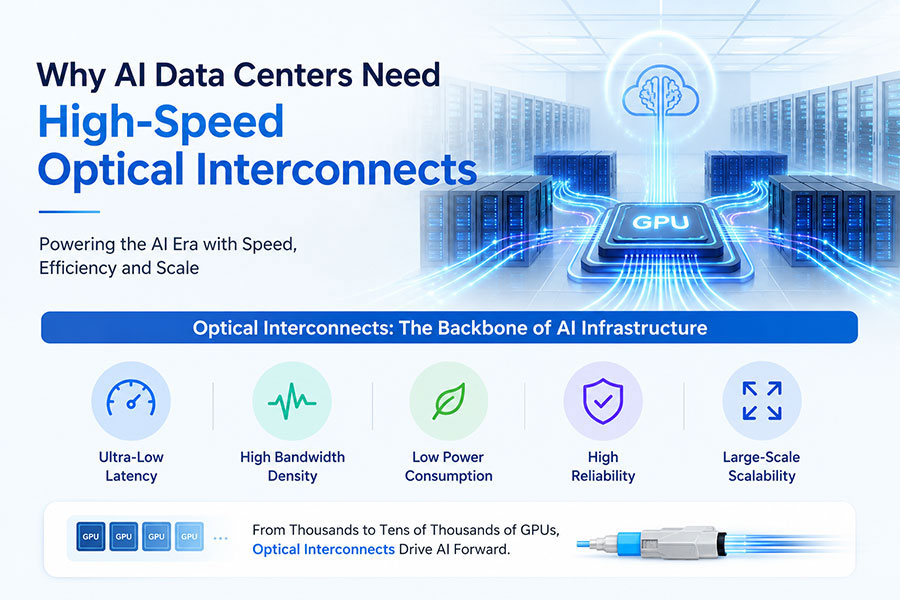

The rapid expansion of cloud computing and AI applications is driving unprecedented growth in global data center infrastructure, intensifying the demand for communication solutions with higher bandwidth and lower latency. High-speed optical modules, such as 400G, 800G, and emerging 1.6T variants, have become critical enablers for intra-data center connections and inter-facility links. These components not only support compute-intensive workloads like AI training and large-scale simulations but also ensure seamless data transfer across cloud, edge, and endpoint layers. Furthermore, the technology lifecycle has significantly accelerated: the industry transitioned from 100G to 800G within just a few years, with 1.6T transceivers poised for widespread commercial deployment. This condensed development cycle is compelling leading suppliers to continuously propel innovation to keep pace with market expectations and evolving architectural requirements.

As data rates advance beyond 800G towards 1.6T and higher, traditional pluggable modules face increasingly severe challenges regarding power consumption and front-panel density. These physical limitations are driving the industry's shift towards solutions with higher integration levels. Co-Packaged Optics (CPO) and Near-Packaged Optics (NPO) represent a fundamental architectural shift by relocating the optical engine closer to or directly integrating it with the switch ASIC. This integration can substantially reduce power consumption by minimizing circuit trace losses and achieve a revolutionary improvement in port density, thereby addressing critical bottlenecks for next-generation AI clusters and hyperscale data centers.

Leveraging the unique advantages of mature CMOS processes, silicon photonics technology demonstrates significant potential in integration level, power consumption, and cost-effectiveness, establishing itself as a key technological path to meet the demands of high-speed, high-density data centers. As production capacity for 800G/1.6T optical modules gradually increases, silicon photonics solutions are being increasingly deployed in AI clusters and hyperscale data centers, becoming a vital force driving technological iteration and reshaping the competitive landscape.

The raw material cost structure of AI optical modules primarily includes optical components, integrated circuit chips, printed circuit boards (PCB), and others (housing and miscellaneous components). Among these, optical components constitute the most significant portion, accounting for 74% of the total module cost. Integrated circuit chips also represent a relatively substantial share, approximately 19%.

The optical module market is characterized by exceptionally high technological barriers to entry in advanced fields such as silicon photonics, low-power high-speed optical communication, and high-density integration. These areas require multidisciplinary expertise spanning materials science, optoelectronic integration, advanced packaging, and microelectronics. Companies that pioneer the launch of next-generation products typically gain a significant first-mover advantage, necessitating sustained R&D investment and the capability to keep pace with rapid technological evolution.

The optical module industry operates within a globalized market landscape, requiring participants to establish an international presence in R&D, manufacturing, and sales operations. Leading companies maintain their competitive edge through localized service capabilities and global logistics networks, enabling them to respond swiftly to diverse regional demands. Establishing such global infrastructure not only requires substantial capital investment but also mature management systems, operational expertise, and long-term customer partnerships—resources that cannot be quickly replicated.

>

>

>

>

>

>

>

>

>

>

>

>